Quick Takes

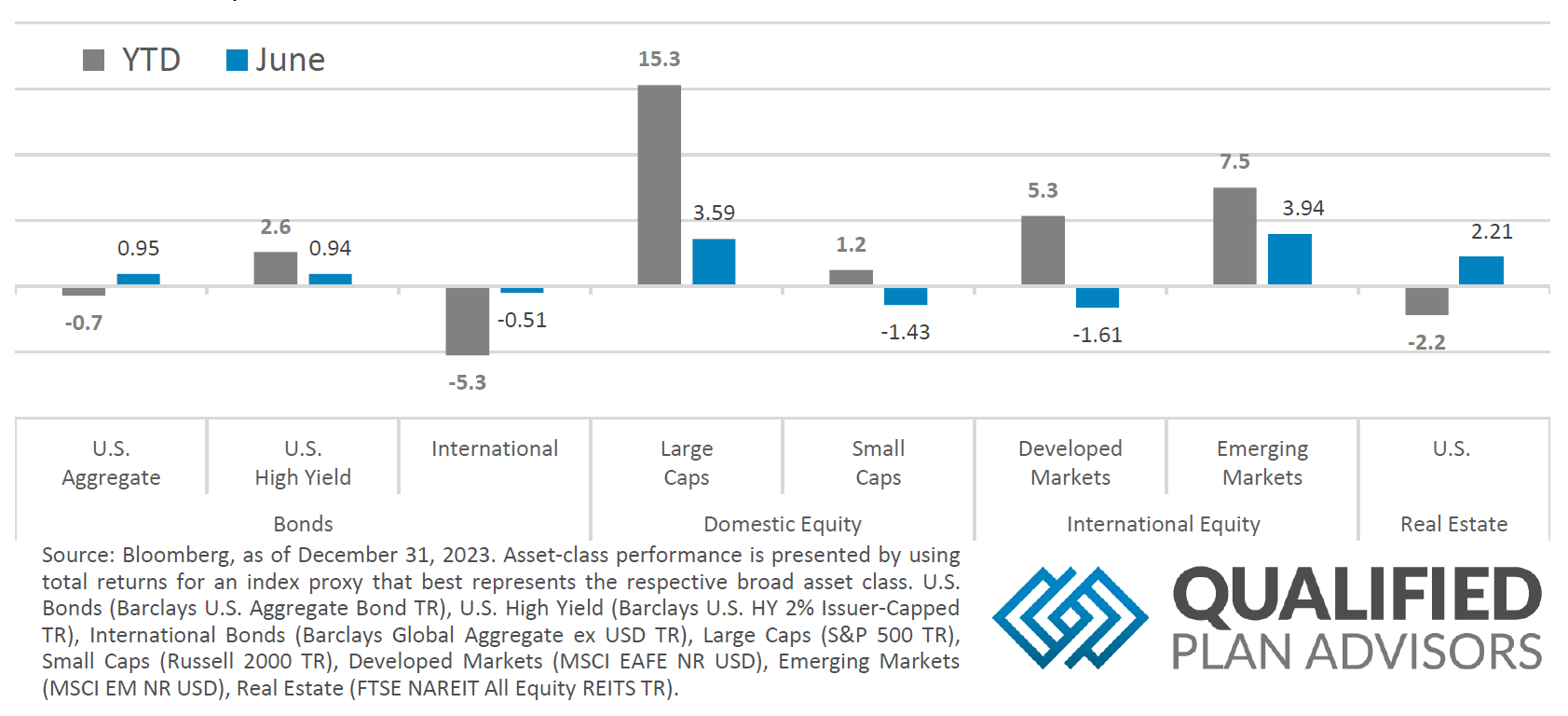

- Risk Assets Drift Up. For the month of June, risk assets saw some upward momentum, especially in Large Caps and Emerging Markets, but International Equities and Small Caps had a tougher go for the month.

- Inflation Continued Softening. Inflation, as measured by the Fed’s preferred metric of PCE Deflator, showed some promising signs of price pressures easing. While encouraging, Fed rhetoric suggests that they will be patient before transitioning to a looser monetary policy.

- King Dollar. The dollar climbed sharply higher throughout the month of June, especially as other Central Banks eased their respective tightening of monetary policies, leaving the USD as one of the globe’s higher-yielding currencies.

- Personal Spending and Labor Markets. Personal Spending showed robust signs in the June reading for the month of May and Labor Markets showed continued resiliency but might be nearing an inflection point. With Labor Markets continuing to show signs of strength, it’s of little surprise that wages posted a respectable uptick in the June data reading.

Asset Class Performance

Large Caps continued their melt up for the month of June, with Emerging Markets being the only major asset class to outperform. Other major asset classes posted a more modest return, save for Small Caps and Developed International Equities, which were in the red for the month.

Markets & Macroeconomics

Markets & Macroeconomics

Like the incoming summer weather, Consumer Spending showed signs of heating up for the month of May. Some of this increase may be a seasonal effect due to increased travel as the school year winds down, but the bump up in May was an encouraging sign after April’s lackluster data. Thus far, consumers have been the hero of the U.S. economy, and arguably the global economy, throughout the Fed’s tightening cycle as they battle entrenched Inflation back to their long-term target range. While consumer spending showed signs of warming up, Inflation, as measured by the Fed’s preferred metric of Core PCE, landed in line with market expectations of +0.1% for May. The headline data release gets rounded to 1 decimal point but on an unrounded basis, the metric was up +0.08%. This was the smallest advance since November 2020. With Inflation showing continuing signs of easing as the year goes on, this could lead to a path for the Fed to start loosening monetary policy via their first interest rate cut since the tightening cycle began. Possibly even more encouraging, combining easing Inflation with the recovery in Consumer Spending also opens the doorway to the Fed accomplishing what many market participants thought was impossible by successfully taming Inflation while preventing the U.S. economy from entering a recessionary period. Putting all of this together, the May economic data readings came out largely positive, but by no means does one reading make a trend. The Fed has reiterated multiple times in its collective rhetoric that members intend to be patient and look for sustained trends Inflation is showing persistent signs of cooling off before they begin to ease financial conditions

Bottom Line: The Fed’s preferred Inflation metric for the month of May showed one of the smallest increases since November 2020. This positive reading buoys support for a rate cut later this year and that it may come sooner than some market participants were expecting. While the May data reading was positive, it is likely not enough to completely solidify the case to ease financial conditions and the continued Fed rhetoric leans more towards patience from the members until they have seen sustained signs from the data that Inflation has been wrestled into submission. While Inflation painted a possible picture of the economy slowing, Consumer Spending, ticked up in the month of May. If Consumer Spending remains robust throughout the summer months while Inflation shows continued easing pressure, the Fed may be able to accomplish what many market participants thought was near impossible; getting Inflation back to their target range without sending the U.S. into a recession.

Download the full review.

©2024 Prime Capital Investment Advisors, LLC. The views and information contained herein are (1) for informational purposes only, (2) are not to be taken as a recommendation to buy or sell any investment, and (3) should not be construed or acted upon as individualized investment advice. The information contained herein was obtained from sources we believe to be reliable but is not guaranteed as to its accuracy or completeness. Investing involves risk. Investors should be prepared to bear loss, including total loss of principal. Diversification does not guarantee investment returns and does not eliminate the risk of loss. Past performance is no guarantee of comparable future results.

Source: Sources for this market commentary derived from Bloomberg Asset-class performance is presented by using market returns from an exchange‐traded fund (ETF) proxy that best represents its respective broad asset class. Returns shown are net of fund fees for and do not necessarily represent performance of specific mutual funds and/or exchange-traded funds recommended by the Prime Capital Investment Advisors. The performance of those funds June be substantially different than the performance of the broad asset classes and to proxy ETFs represented here. U.S. Bonds (iShares Core U.S. Aggregate Bond ETF); High‐Yield Bond (iShares iBoxx $ High Yield Corporate Bond ETF); Intl Bonds (SPDR® Bloomberg Barclays International Corporate Bond ETF); Large Growth (iShares Russell 1000 Growth ETF); Large Value (iShares Russell 1000 Value ETF); Mid Growth (iShares Russell Mid-Cap Growth ETF); Mid Value (iShares Russell Mid-Cap Value ETF); Small Growth (iShares Russell 2000 Growth ETF); Small Value (iShares Russell 2000 Value ETF); Intl Equity (iShares MSCI EAFE ETF); Emg Markets (iShares MSCI Emerging Markets ETF); and Real Estate (iShares U.S. Real Estate ETF). The return displayed as “Allocation” is a weighted average of the ETF proxies shown as represented by: 30% U.S. Bonds, 5% International Bonds, 5% High Yield Bonds, 10% Large Growth, 10% Large Value, 4% Mid Growth, 4% Mid Value, 2% Small Growth, 2% Small Value, 18% International Stock, 7% Emerging Markets, 3% Real Estate.

Advisory products and services offered by Investment Adviser Representatives through Prime Capital Investment Advisors, LLC (“PCIA”), a federally registered investment adviser. PCIA: 6201 College Blvd., Suite#150, Overland Park, KS 66211. PCIA doing business as Prime Capital Wealth Management (“PCWM”) and Qualified Plan Advisors (“QPA”). Securities offered by Registered Representatives through Private Client Services, Member FINRA/SIPC. PCIA and Private Client Services are separate entities and are not affiliated.

© 2024 Prime Capital Investment Advisors, 6201 College Blvd., Suite #150, Overland Park, KS 66211.