Quick Takes

- Risk Assets Melt Up. Market participants continued right where November left off with almost all major asset classes continuing to melt up for the month of December, locking in a gain for 2023 across the board.

- Inflation Continued Softening. Inflation, as measured by the Fed’s preferred metric of PCE Deflator, continued to show signs of softening through the month of November, landing at +2.6% versus estimates of +2.8% on the year-over-year metric.

- Greenback Softens With Inflation. The dollar was largely in a state of decline against other major currencies for the month of December with market participants pricing in future rate cuts.

- Personal Consumption and Labor Markets. Personal Consumption for the third quarter was revised lower from +3.6% to +3.1%. Labor Markets gave off mixed signals with the Job Openings and Labor Turnover Survey “JOLTS” coming in below expectations of 9.3 million, at 8.7 million for the month of October, but the Unemployment Rate for November came in below expectations of 3.9%, coming in at 3.7%.

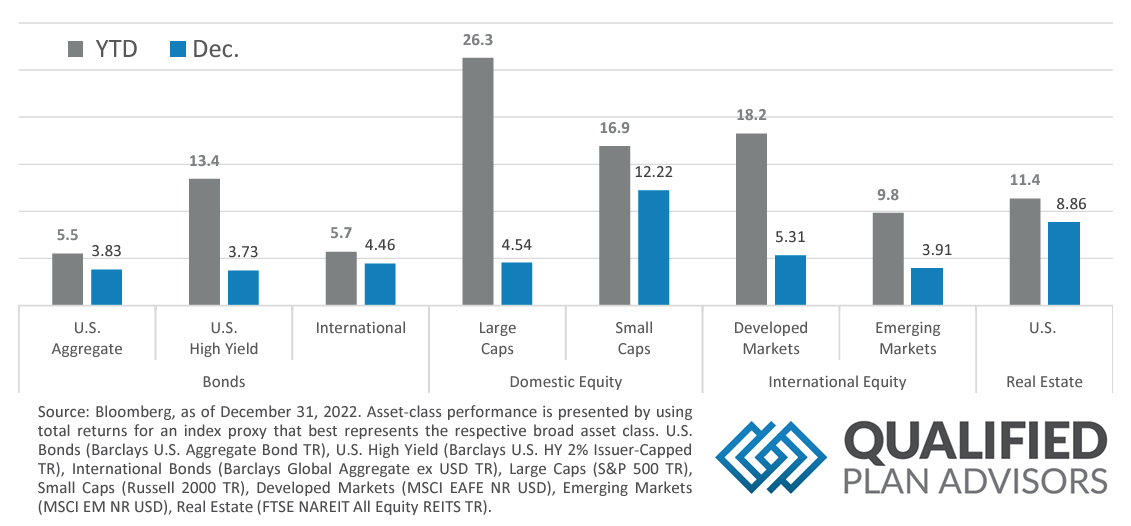

Asset Class Performance

Risk Assets posted a strong December with Small Cap equities posting over a +12% increase for the month. With a solid December in the books, most major risk asset classes solidified a respectable year-to-date return well into the green, led by Large Cap equities posting over a 26% return for 2023.

Markets & Macroeconomics

The Job Openings and Labor Turnover Survey (“JOLTS”), a measure of employers searching for workers in the United States, showed signs of softening in the December reading for the month of October, coming in below expectations of 9.3 million at 8.73 million. A more recent measure of Labor Markets showed a surprise strengthening with the US economy adding +199,000 jobs in the month of November above market expectations of 185,000, which led to the Unemployment rate falling to 3.7%. Digging into the underlying data, a piece of the increase was due to the resolution of the United Auto Workers strike, additionally, areas of increase included health care, leisure and hospitality, and government hiring. Surprisingly, despite heading into the holiday rush season, retail was one of the categories that showed a decline in the data reading. In most scenarios, a strong labor market is something that many market participants would cheer on, however, with the Fed continuing the path of attempting to tame demand and ultimately inflation, a strong labor market typically leads to strong wage growth. With compensation for employees continuing to show signs of strength, this will likely lead to Consumer Spending remaining resilient. So far, consumers have been the hero throughout the Fed’s tightening campaign with their spending habits preventing the US economy from slipping into a contractionary period. However, despite the recent resiliency in wage growth, consumers might be showing signs of spending fatigue with official data releases surrounding Consumer Spending data coming in softer than expected recently. This softening of spending habits may be temporary cutbacks in anticipation of the upcoming holiday season or consumers could be feeling the pressure of higher prices impacting their savings accounts and short-term credit facilities. With how important consumers are to the US economy, market participants will likely keep a close eye on spending habits in the coming months.

Bottom Line: Labor markets showed surprising resiliency into the final month of the year with the Unemployment Rate falling to 3.7% after the US economy added 199,000 jobs in the month of November. With the labor markets strengthening through the month of November, it’s of little surprise that Wage Growth was strong as well. Typically, when Wage Growth is strong, this leads to strong Consumer Spending. Consumers have been in spending mode for the majority of the year but might be showing signs of fatigue with official government data releases surrounding Consumer Spending coming in softer than expected recently.

©2023 Prime Capital Investment Advisors, LLC. The views and information contained herein are (1) for informational purposes only, (2) are not to be taken as a recommendation to buy or sell any investment, and (3) should not be construed or acted upon as individualized investment advice. The information contained herein was obtained from sources we believe to be reliable but is not guaranteed as to its accuracy or completeness. Investing involves risk. Investors should be prepared to bear loss, including total loss of principal. Diversification does not guarantee investment returns and does not eliminate the risk of loss. Past performance is no guarantee of comparable future results.

Source: Bloomberg. Asset‐class performance is presented by using market returns from an exchange‐traded fund (ETF) proxy that best represents its respective broad asset class. Returns shown are net of fund fees for and do not necessarily represent performance of specific mutual funds and/or exchange-traded funds recommended by the Prime Capital Investment Advisors. The performance of those funds June be substantially different than the performance of the broad asset classes and to proxy ETFs represented here. U.S. Bonds (iShares Core U.S. Aggregate Bond ETF); High‐Yield Bond (iShares iBoxx $ High Yield Corporate Bond ETF); Intl Bonds (SPDR® Bloomberg Barclays International Corporate Bond ETF); Large Growth (iShares Russell 1000 Growth ETF); Large Value (iShares Russell 1000 Value ETF); Mid Growth (iShares Russell Mid-Cap Growth ETF); Mid Value (iShares Russell Mid-Cap Value ETF); Small Growth (iShares Russell 2000 Growth ETF); Small Value (iShares Russell 2000 Value ETF); Intl Equity (iShares MSCI EAFE ETF); Emg Markets (iShares MSCI Emerging Markets ETF); and Real Estate (iShares U.S. Real Estate ETF). The return displayed as “Allocation” is a weighted average of the ETF proxies shown as represented by: 30% U.S. Bonds, 5% International Bonds, 5% High Yield Bonds, 10% Large Growth, 10% Large Value, 4% Mid Growth, 4% Mid Value, 2% Small Growth, 2% Small Value, 18% International Stock, 7% Emerging Markets, 3% Real Estate.

Advisory products and services offered by Investment Adviser Representatives through Prime Capital Investment Advisors, LLC (“PCIA”), a federally registered investment adviser. PCIA: 6201 College Blvd., Suite#150, Overland Park, KS 66211. PCIA doing business as Prime Capital Wealth Management (“PCWM”) and Qualified Plan Advisors (“QPA”). Securities offered by Registered Representatives through Private Client Services, Member FINRA/SIPC. PCIA and Private Client Services are separate entities and are not affiliated.

© 2023 Prime Capital Investment Advisors, 6201 College Blvd., Suite #150, Overland Park, KS 66211.